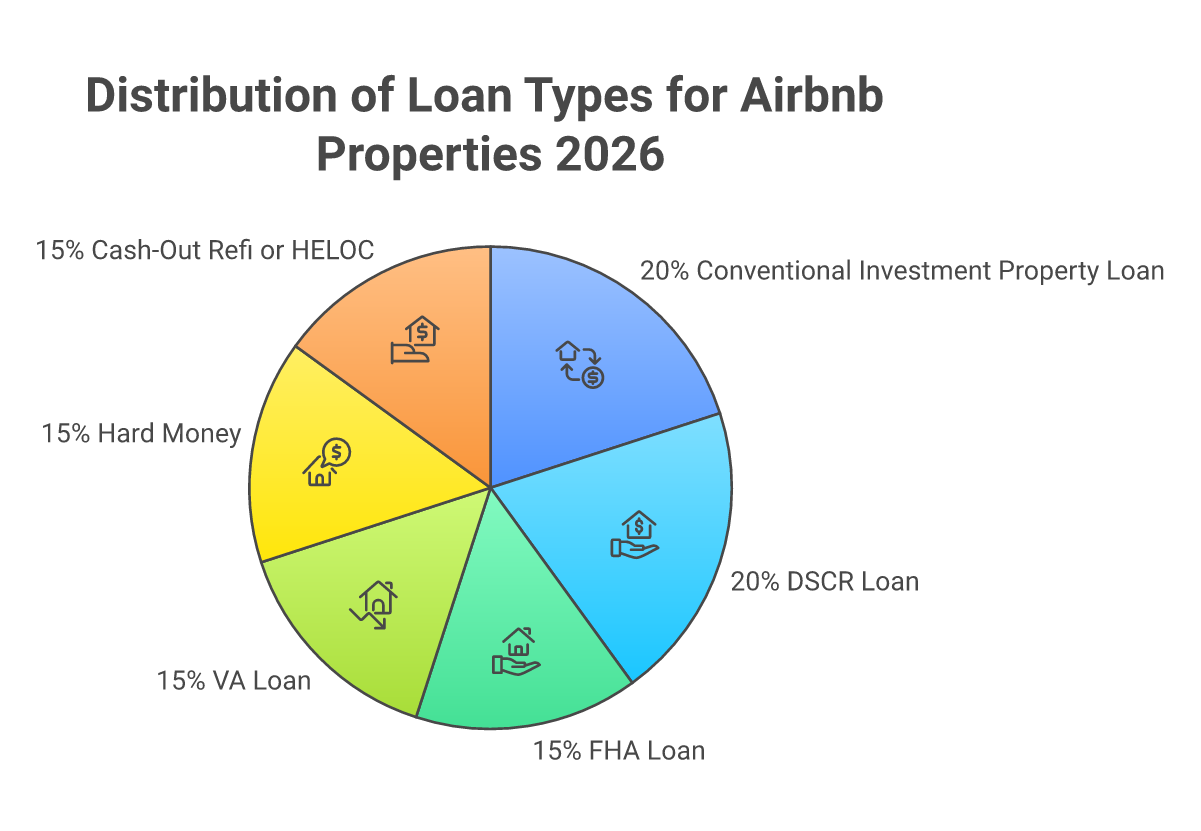

An Airbnb loan is not a single official product. It is shorthand for any financing used to buy or operate a short term rental property. Six main loan types fund Airbnb investments in 2026: conventional investment property mortgages (Fannie Mae, 15% to 25% down, requires personal income qualification), DSCR loans (qualified by projected rental income, not personal income, 20% to 25% down), FHA loans (3.5% down but only for owner-occupied house hacking), VA loans (zero down for eligible veterans on owner-occupied), hard money loans (short-term bridge financing, 10% to 18% rates), and cash-out refinance plus HELOC against existing home equity. Most airbnb investors use a DSCR loan or a conventional investment property mortgage. DSCR is the easier qualification path because the lender underwrites the rental income, not your personal income. The 10XBNB system operates 24 properties without traditional financing through rental arbitrage, but for buyers, financing typically requires $40,000 to $80,000+ in down payment plus closing costs on a $300,000 unit.

What Is an Airbnb Loan?

The phrase “airbnb loan” is shorthand, not an official mortgage product. No lender markets a loan branded specifically for Airbnb listings. What hosts mean when they search for an Airbnb loan is the type of financing they need to buy or operate a short term rental property. The Airbnb platform itself does not issue loans to hosts.

The financing decision splits into two paths. Path 1: you want to buy a property and list it on Airbnb. This requires an investment property loan because the property is not your primary residence. Path 2: you want capital to start a rental arbitrage business (lease and re-list, no purchase). This typically uses business credit lines, personal savings, or partner capital, not a property loan.

For owners, six main loan types fund Airbnb property purchases in 2026. Each has a different qualification path, down payment requirement, and interest rate range. The right loan depends on whether the property will be owner-occupied (you live there), how much cash you can put down, and how strong your personal income qualifies.

The 6 Loan Types That Finance Airbnb Properties

1. Conventional Investment Property Loan (Fannie Mae / Freddie Mac)

The standard option for buying a non-owner-occupied rental property. Conventional investment property loans follow Fannie Mae and Freddie Mac underwriting guidelines. They require 15% to 25% down payment (most lenders prefer 25% for investment properties), credit scores of 680+ (720+ for the best rates), and full personal income documentation through W-2s, tax returns, and bank statements.

Per the FHFA’s 2026 Conforming Loan Limit announcement, the standard conforming loan limit for one-unit properties is $832,750 in most U.S. counties as of January 1, 2026. High-cost areas (Hawaii, Alaska, parts of California, New York, etc.) have higher limits. Conventional loans above the conforming limit are jumbo loans with stricter qualification.

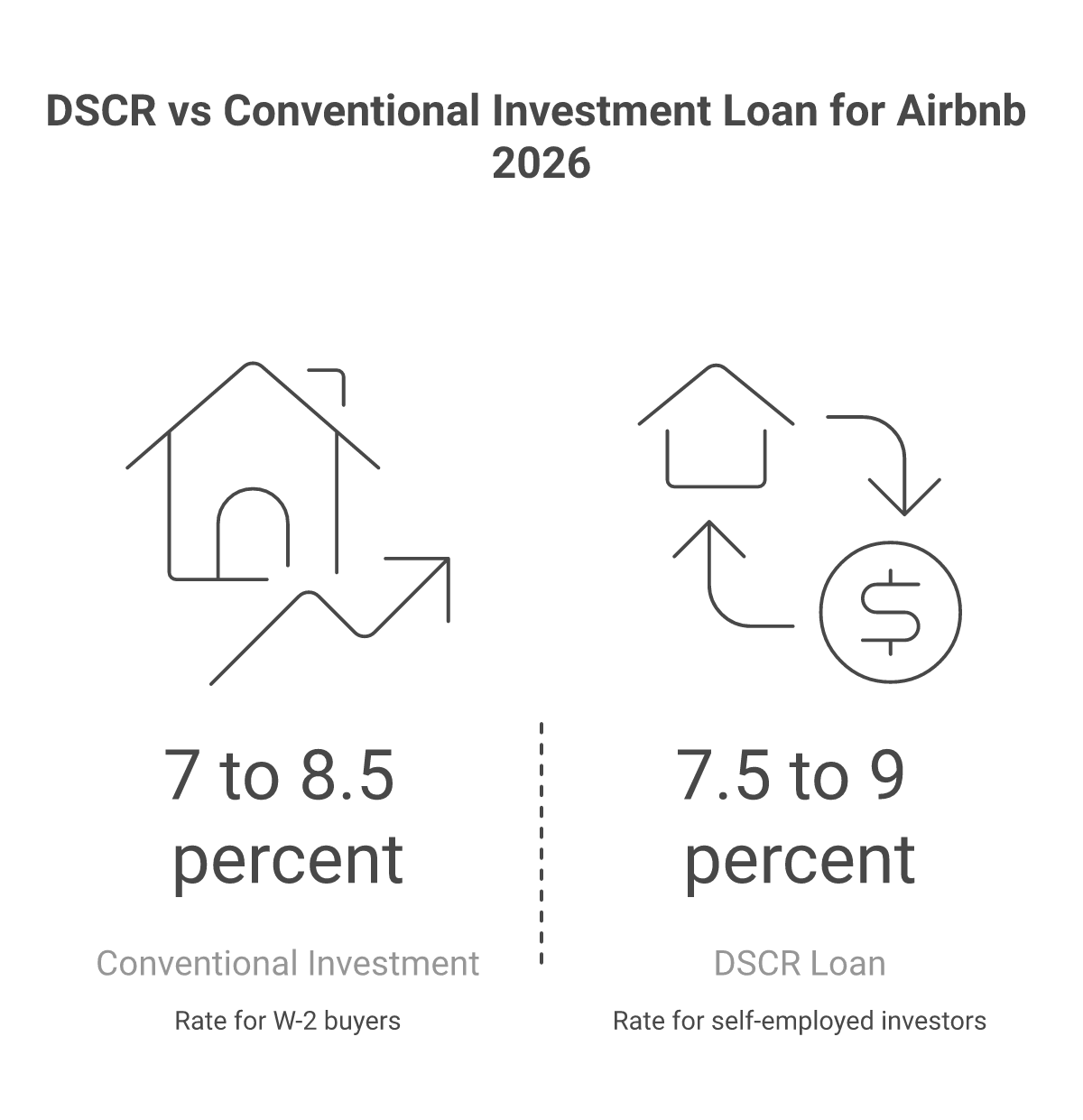

Interest rates on conventional investment property loans typically run 0.5% to 1.0% higher than primary residence rates because of the higher lender risk. Expect rates in the high 7% to mid 8% range as of mid-2026, though rates shift weekly with Treasury yields.

2. DSCR Loan (Debt Service Coverage Ratio)

The most popular Airbnb loan for serious investors. DSCR loans are qualified by the property’s projected rental income, not by the borrower’s personal income. The lender calculates the Debt Service Coverage Ratio: projected monthly rent divided by total monthly mortgage payment (principal, interest, taxes, insurance, HOA). A DSCR of 1.0 means rental income exactly covers the mortgage. Most DSCR lenders require 1.0 to 1.25 minimum.

DSCR loans are perfect for self-employed buyers, real estate investors with multiple properties, and Airbnb operators whose tax returns show low W-2 income but strong projected rental cash flow. Typical terms: 20% to 25% down payment, 640+ credit score, 7% to 9% interest rate (slightly higher than conventional), 30-year fixed amortization.

Top DSCR lenders for Airbnb investors in 2026 include Visio Lending, Kiavi (formerly LendingHome), Lima One Capital, and Easy Street Capital. Each lender has different DSCR requirements, rate sheets, and property-type restrictions for short term rentals.

3. FHA Loan (Owner-Occupied House Hacking)

Only viable if you plan to LIVE in the property while listing rooms on Airbnb (house hacking). FHA loans require 3.5% down for borrowers with 580+ credit scores. The property must be your primary residence for at least 12 months. You can list spare rooms or a separate unit on Airbnb during that period.

The trade-off: FHA loans cap at the conforming loan limit ($832,750 in most areas per FHFA 2026), require mortgage insurance for the life of the loan unless you put 10%+ down, and limit you to one FHA loan at a time. The 3.5% down payment is the lowest entry point for any Airbnb financing strategy.

4. VA Loan (Eligible Veterans, Owner-Occupied)

If you are an eligible active-duty military member, veteran, or surviving spouse, the VA loan is the strongest financing option available. Zero down payment, no PMI, no upfront mortgage insurance, and competitive interest rates. The catch: VA loans are strictly for owner-occupied primary residences. You must live in the property for at least 12 months before converting it to a full short term rental.

Most veterans who use VA loans for Airbnb either house hack (live in part of a multi-unit while renting other units on Airbnb) or live in the property for 12 months and then convert to a full rental while moving to a second VA-financed property.

5. Hard Money Loan (Short-Term Bridge Financing)

Hard money loans are short-term (6 to 24 months), high-rate (10% to 18%), asset-based loans from private lenders. They fund 70% to 80% of the property’s after-repair value, qualify on the property and the borrower’s experience rather than personal income, and close in 7 to 21 days vs 30 to 45 days for conventional.

Most Airbnb investors use hard money for fix-and-flip deals or to acquire a property quickly when conventional financing would take too long. The high interest rate makes hard money a poor long-term option. The standard pattern: close with hard money, fix and stabilize the property, then refinance into a DSCR or conventional loan within 12 months.

6. Cash-Out Refinance and HELOC (Equity From Existing Home)

If you already own a home with equity, a cash-out refinance or HELOC (home equity line of credit) lets you pull capital from your existing property to fund an Airbnb purchase. Cash-out refi replaces your current mortgage with a larger one and gives you the difference as cash. HELOC opens a revolving credit line against your home’s equity.

Cash-out refi rates run similar to conventional mortgage rates (currently 7% to 8.5%). HELOC rates are variable, usually prime + 0.5% to 2.5%. Both carry the risk of using your primary residence as collateral. If the Airbnb investment fails, your home is on the line. Most successful airbnb investors use this strategy only for their second or third property, not their first.

Loan Comparison Table

| Loan type | Down payment | Min credit | Best for |

|---|---|---|---|

| Conventional investment | 15% to 25% | 680 | W-2 buyers with strong personal income |

| DSCR loan | 20% to 25% | 640 | Self-employed, multi-property investors |

| FHA (owner-occupied) | 3.5% | 580 | House hacking, first-time buyers |

| VA (eligible veterans) | 0% | 580 to 620 (lender-set) | Veterans, active duty, surviving spouses |

| Hard money | 20% to 30% | No minimum (asset-based) | Fast-close situations, fix-and-flip |

| Cash-out refi / HELOC | N/A (uses existing equity) | 680 typical | Owners with substantial home equity |

Lender Requirements: How to Qualify for an Airbnb Loan

Six factors drive whether you qualify for an Airbnb loan and what rate you get.

1. Credit score. Minimum 580 for FHA and VA, 640 for DSCR, 680 for conventional investment. The 720+ tier unlocks the best rates. Pull your credit report from AnnualCreditReport.com (the only federally authorized free credit report site) 60 to 90 days before applying so you can clean up errors and pay down revolving balances.

2. Down payment and reserves. Conventional and DSCR lenders typically require 20% to 25% down for an Airbnb investment property. On top of the down payment, lenders want 2 to 6 months of mortgage payments in reserves as proof you can cover void periods. On a $300,000 property, that means $60,000 to $75,000 down plus $10,000 to $20,000 in reserves.

3. Debt-to-income ratio (DTI). For conventional loans, DTI must be below 45%. DSCR loans skip DTI entirely because they qualify on rental income. If your personal DTI is high (student loans, car loans, credit card balances), DSCR is the easier path.

4. Rental income projection (DSCR specific). Most DSCR lenders use Form 1007 (Single-Family Comparable Rent Schedule) or AirDNA Rentalizer data to project rental income. A higher projected rent improves your DSCR and qualifies you for better rates. Some DSCR lenders accept short term rental income projections; others require long term lease comps. Confirm with each lender before applying.

5. Property type and condition. Single-family homes, 2-to-4-unit properties, and condos qualify for most loan programs. Mobile homes, log cabins, and “non-warrantable” condos (less than 50% owner-occupancy in the building) often require specialty lenders. The property must pass an appraisal and inspection.

6. Experience. First-time investors face stricter underwriting than experienced operators. Some DSCR lenders and most hard money lenders give better terms to borrowers with 2+ prior investment properties.

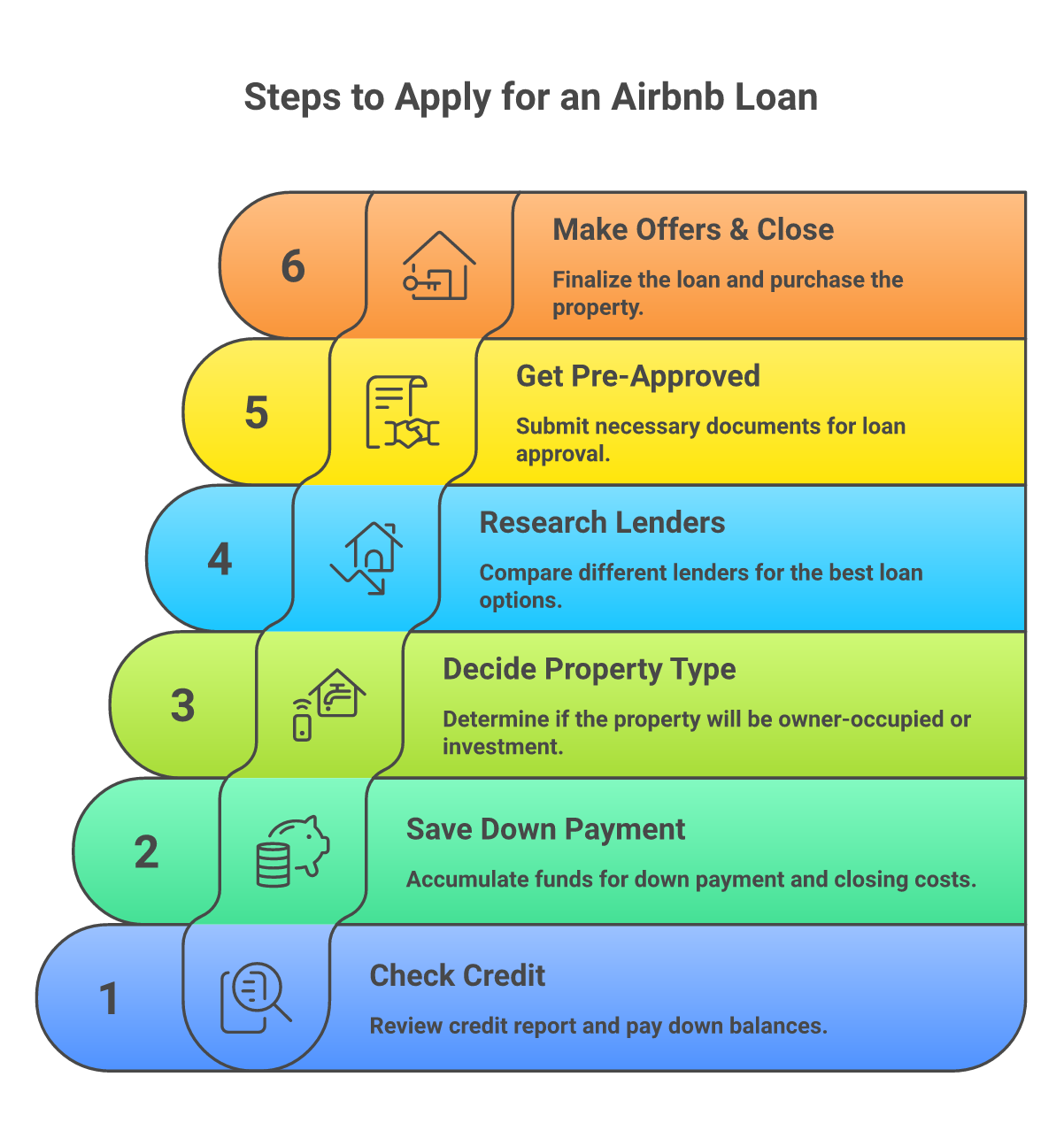

Step-by-Step: How to Apply for an Airbnb Loan

Step 1: Check Your Credit and Finances

Pull your credit report from AnnualCreditReport.com. Pay down revolving credit card balances to under 30% of limits (this single move can boost your score 20 to 50 points within 60 days). Make sure all bills paid on time for the prior 12 months. Calculate your DTI: total monthly debt payments divided by gross monthly income.

Step 2: Save Your Down Payment + Reserves

Plan for 25% down on the target property purchase price plus 2 to 6 months of mortgage reserves plus closing costs (typically 2% to 5% of purchase price). On a $300,000 property, that totals $77,000 to $95,000 in cash needed at closing.

Step 3: Decide Owner-Occupied or Investment

If you can live in the property for 12 months while listing rooms on Airbnb, FHA (3.5% down) or VA (0% down for veterans) unlocks the cheapest financing. If the property is purely an investment, choose between conventional investment, DSCR, or hard money based on your personal income strength.

Step 4: Research and Compare Lenders

For conventional investment, work with national mortgage brokers or local credit unions. For DSCR, contact Visio Lending, Kiavi, Lima One Capital, and Easy Street Capital for rate quotes. For hard money, check local real estate investor meetups and online platforms like LendingTree or RCN Capital. Always get quotes from 3+ lenders.

Step 5: Get Pre-Approved

Pre-approval involves submitting a full loan application package: 2 years tax returns, 2 months bank statements, paystubs (if W-2 employed), personal financial statement, credit report. The lender issues a pre-approval letter for a specific loan amount, which you use when making offers on properties.

Step 6: Make Offers and Close

Submit offers on properties using the pre-approval letter. Once an offer is accepted, the lender orders an appraisal and inspection. Underwriting takes 2 to 4 weeks for conventional, 1 to 3 weeks for DSCR, and 5 to 14 days for hard money. Final closing requires a wire transfer for the down payment plus closing costs and signing 50+ pages of loan documents.

The Top Lenders for Airbnb Loans in 2026

Loan terms shift weekly, so always confirm current rates and requirements directly with the lender. As of mid-2026, these lenders are most commonly used by Airbnb investors.

For DSCR Loans

- Visio Lending. One of the largest DSCR lenders in the US. Specializes in short term rental loans. Typical terms: 20% to 25% down, 640+ credit, $75K minimum loan.

- Kiavi (formerly LendingHome). Strong digital experience. Offers DSCR plus fix-and-flip bridge loans. Typical terms: 20% to 25% down, 660+ credit.

- Lima One Capital. Investor-focused lender. Offers DSCR and bridge products. Typical terms: 20% down, 680+ credit.

- Easy Street Capital. DSCR specialty for short term rental investors. Will underwrite based on STR projection data from AirDNA.

For Conventional Investment

- Local credit unions. Often offer the lowest rates for borrowers who already bank with them. Worth a quote even if you plan to use a broker.

- National lenders. Rocket Mortgage, Wells Fargo, Chase, and PennyMac all offer conventional investment property loans. Rates are competitive but service varies by region.

- Mortgage brokers. Can shop multiple wholesale lenders at once. Add a small fee but often find better rates than direct lenders for non-prime borrowers.

For SBA Loans

Most Airbnb properties do not qualify for SBA loans because the SBA generally excludes financing for passive real estate investment. However, SBA loans can fund the operating side of an Airbnb business (working capital, furniture, software, business credit lines). For details, see the SBA loan programs overview. The SBA 7(a) and microloan programs are the most accessible for small Airbnb operators.

Financing Rental Arbitrage vs Owning

The financing question for rental arbitrage hosts is very different from property owners. Rental arbitrage operators do not buy property, so they do not need mortgages or investment property loans. Their capital need is the startup investment for furniture, deposits, and operating reserve, typically $7,000 to $15,000 per unit per our Airbnb startup cost guide.

Rental arbitrage hosts typically fund these startup costs through personal savings, business credit cards (Chase Ink Business Preferred, Capital One Spark Cash for Business, American Express Business), small business lines of credit from local banks, or partnership capital from investors who fund the unit in exchange for revenue share.

The advantage of the rental arbitrage path: no down payment required, fast scaling, no risk of personal foreclosure if the business fails. The disadvantage: no equity buildup, no depreciation tax benefit, and the property owner can refuse to renew the lease. For the full rental arbitrage launch playbook, see our rental arbitrage strategy guide. For the deal math before signing any lease, run the numbers through our free Airbnb arbitrage calculator.

Common Airbnb Loan Mistakes

1. Applying for too many loans at once. Each hard credit pull lowers your score by 2 to 5 points and stays on your report for 2 years. Group all loan applications within a 14 to 45 day window so the credit bureaus count them as a single inquiry.

2. Lying about owner-occupancy status. Some buyers tell lenders they will live in the property to qualify for owner-occupied rates (FHA, VA, conventional primary residence) and then convert to short term rental immediately. This is mortgage fraud and a federal crime. Lenders verify occupancy through property tax records, utility bills, mail addresses, and inspections.

3. Underestimating closing costs. Closing costs run 2% to 5% of purchase price (lender fees, title insurance, appraisal, recording fees, transfer taxes, prepaid escrow). On a $300,000 property, plan for $6,000 to $15,000 in closing costs on top of the down payment.

4. Skipping the property inspection. Investment property buyers sometimes waive inspection to win competitive bids. This is a $5,000 to $50,000 mistake when the roof, HVAC, or foundation needs replacement post-close. Never skip the inspection, even on cash deals.

5. Forgetting short term rental insurance. Your homeowners insurance does not cover short term rental use. Most lenders require proof of short term rental insurance at closing on an investment property. Plan for $80 to $250 monthly per unit for a proper short term rental policy.

Tax Treatment of Airbnb Loan Interest

Mortgage interest on an Airbnb investment property is fully deductible against rental income, per IRS Schedule E instructions. You also deduct property taxes, depreciation, repairs, insurance, and operating expenses. The combination typically produces a tax loss in early years that can offset other passive income.

The math: a $300,000 property at 8% interest with 25% down pays roughly $16,500 in mortgage interest in year one. Combined with $9,000 in property tax, $10,000 in depreciation (residential rental property depreciates over 27.5 years), $4,000 in repairs and operating costs, the property produces a $39,500 paper loss on the tax return even when cash flow is positive. This is one of the biggest reasons real estate investors prefer ownership to rental arbitrage on a long-term basis.

Consult a CPA experienced with short term rentals before claiming any of these deductions. The IRS has specific “material participation” rules that determine whether passive losses can offset W-2 income. Your CPA will know the local case law.

Frequently Asked Questions

Can you use a regular mortgage for an Airbnb?

Yes, if it is a conventional investment property mortgage (15% to 25% down, 680+ credit, qualified by personal income). You cannot use a conventional primary residence mortgage and convert it to an Airbnb without violating the loan terms. FHA and VA loans require owner-occupancy for at least 12 months before full short term rental conversion. The DSCR loan path skips personal income qualification and is the most popular Airbnb loan for serious investors.

What credit score do I need for an Airbnb loan?

Minimum 580 for FHA loans (owner-occupied house hacking). 640 for DSCR loans. 680 for conventional investment property loans. 720+ unlocks the best rates across all categories. Hard money lenders have no formal credit minimum because they qualify on the property’s value and the borrower’s experience.

How much do I need to put down on an Airbnb property?

3.5% for FHA owner-occupied. 0% for VA-eligible veterans. 15% to 25% for conventional investment (most lenders prefer 25%). 20% to 25% for DSCR loans. 20% to 30% for hard money. Plus closing costs of 2% to 5% of purchase price. Plus 2 to 6 months of mortgage payments in reserves. On a $300,000 property, plan for $77,000 to $95,000 total cash needed at closing.

Is a DSCR loan better than a conventional loan for Airbnb?

DSCR loans are better for buyers with low personal income but strong projected rental income. They skip personal income qualification entirely. Conventional investment loans are better for buyers with strong W-2 income who want the lowest rates. DSCR rates run 0.5% to 1.5% higher than conventional. For most Airbnb investors with 2+ properties or self-employed income, DSCR is the more practical path.

Can I get an SBA loan for an Airbnb?

Usually not for the property purchase itself. The SBA generally excludes passive real estate investment from its loan programs. However, SBA 7(a) and microloan programs can fund the operating side of an Airbnb business: working capital, furniture, software, business credit lines, and equipment. Operators running rental arbitrage businesses are more likely to qualify for SBA financing than property buyers.

Can I refinance an Airbnb loan later?

Yes. Most Airbnb investors refinance within 2 to 5 years of purchase to capture lower rates or pull cash out for the next acquisition. Hard money loans are typically refinanced into DSCR or conventional within 6 to 12 months. Cash-out refinance lets you tap the equity buildup once the property appreciates or the principal pays down.

What are airbnb loan rates in 2026?

As of mid-2026, conventional investment property rates run high 7% to mid 8%. DSCR loans run 7.5% to 9%. FHA owner-occupied rates are about 0.5% lower than conventional. VA loans typically match or beat conventional. Hard money rates remain 10% to 18% for short-term financing. Rates shift weekly with Treasury yields, so confirm current rates with lenders directly before locking. The Consumer Financial Protection Bureau’s loan options resource covers the underlying mechanics.

The Bottom Line on Airbnb Financing

“Airbnb loan” is shorthand for any financing used to buy or operate a short term rental property. Six main loan types fund Airbnb investments in 2026: conventional investment, DSCR, FHA owner-occupied, VA for veterans, hard money for fast closes, and cash-out refi or HELOC against existing equity. The right choice depends on whether you will live in the property, how much cash you can put down, and how strong your personal income qualifies.

For most serious Airbnb investors, DSCR loans are the practical path because they qualify on the property’s projected rental income rather than your personal income. Plan for 20% to 25% down, 640+ credit, plus 2 to 6 months of mortgage reserves. Top DSCR lenders for STR investors include Visio Lending, Kiavi, Lima One Capital, and Easy Street Capital.

If you want to start without buying property, the rental arbitrage path requires only $7,000 to $15,000 per unit in startup costs and skips mortgages entirely. Our rental arbitrage strategy guide covers the full launch playbook. Our 14-step Airbnb business guide walks through the broader business setup including the LLC structure that protects you in either financing path. And our Airbnb LLC formation guide covers how to set up the legal structure most lenders prefer to see.

source https://learn.10xbnb.com/airbnb-loan-financing-guide/

No comments:

Post a Comment