Quick Answer: How to Invest in Short-Term Rentals in 2026

There are four ways to invest in short-term rentals: buy and operate the property yourself, co-list someone else’s property for a revenue share, hire a full-service property management company like Vacasa or Evolve, or place capital in a passive short term rental fund. For high-income W-2 professionals, the highest-return path is buying and self-operating one or two properties while using the OBBBA short-term rental loophole. The 100% bonus depreciation provision restored under the One Big Beautiful Bill Act lets you offset W-2 income with first-year paper losses of $40,000 to $200,000 on a $400,000 property when paired with a cost segregation study. The US short-term rental market is $72 billion in 2025 and growing at 7.4% annually, with cash-on-cash returns of 10 to 15% in well-chosen markets where short-term rentals are still under-supplied.

I started in 2014 with a $65-a-night spare bedroom in my apartment. Twelve years later, I run 24 short-term rentals grossing $175,000 a month. Along the way I’ve watched hundreds of high-income professionals try to copy what worked for me, and a smaller number actually do it. The ones who succeeded had three things in common: they understood there are four very different ways to invest in short-term rentals, they picked the one that fit their capital and time when investing in short-term rentals, and they used the tax code (federal taxes, state taxes, and self-employment taxes) to keep more of what they earned.

This guide is for the W-2 professional making $100K or more (if you work in tech specifically, our companion guides on passive income for software engineers and real estate side income for tech workers drill into your industry-specific math) who is wondering if a short term rental investment is still a real investment in 2026. Short answer: yes, but not the way most YouTube videos sell it. The right way to invest in short term rentals depends on your capital, your time, and how you treat taxes. Long answer below.

Is investing in short-term rentals worth it in 2026?

The US short-term rental market is $72 billion in 2025 and is forecast (per AirDNA market research) to grow at a 7.4% compound annual rate through 2030. That puts it ahead of the broader hotel industry on revenue growth and well ahead of long term rentals on per-night yield. Average occupancy rates across the US vacation rental market sit near 60%, with strong vacation rental markets like Port Arthur Texas hitting 67% (driven by industrial contractor demand from the largest oil refinery in the US plus several multibillion-dollar energy infrastructure projects) and Scottsdale Arizona running 65 to 70% on premium properties. Strong demand persists in mid-size cities and emerging vacation rental markets where the local supply has not caught up to traveler demand.

Cash flow returns of 10 to 15% on cash invested are typical for properties bought right and operated well in 2026. The “bought right” part matters more than people think. The investors I see fail at this investment strategy are not the ones who pick the wrong market. They are the ones who pay too much at purchase, underestimate operating expenses, and then try to make the numbers work with optimistic occupancy rates. Smart short term rental investors do their research with real data before they commit any capital, not after.

Why a short term rental property beats a long term rental on yield

A typical long term rental yields a 6 to 8% gross rental return in most markets. A short term rental on the same property yields 12 to 24% gross rental income when operated well. That is a 2x to 3x revenue uplift on the same investment property. The trade-off is real: a short term rental property requires active operating work, and operating expenses are higher than a long term rental because of cleaning turnovers, supplies, dynamic pricing software, and channel manager subscriptions. The long term rental gives you a less involved investment property; the short term rental property gives you better rental income for the same purchase price.

For high-income professionals, the yield uplift is not the main reason short-term rentals are worth the work in 2026. The tax treatment is. We will cover that in detail below.

What kind of cash flow can you actually expect?

I tell new short term rental investors to model three scenarios on every deal: the proforma case, the realistic case, and the bad year case. On a $400,000 short term rental property in a B-tier market with an average daily rate of $185 and 65% occupancy rates, you are looking at gross revenue around $44,000 a year. After cleaning, supplies, dynamic pricing software, channel manager fees, utilities, insurance, and routine maintenance costs, operating expenses typically run 30 to 35% of gross rental income. Mortgage on $320,000 at current rates is roughly $24,000 a year in interest plus principal. That puts net cash flow somewhere between $5,000 and $9,000 a year on $80,000 of equity, before tax effects.

The cash flow alone is not why you do this. You do this for the appreciation, the tax benefits, and the optional second home use. Stack all four (cash flow, appreciation, tax savings, personal use) and you end up with a real estate investment that compounds faster than dividend portfolios or index funds for the high earner. Add this to a balanced investment portfolio and the diversification value is real: short term rental investments are correlated to travel and consumer spending. Short-term rentals tend to perform when leisure spending is up, not to the equity markets that already dominate most professionals’ net worth.

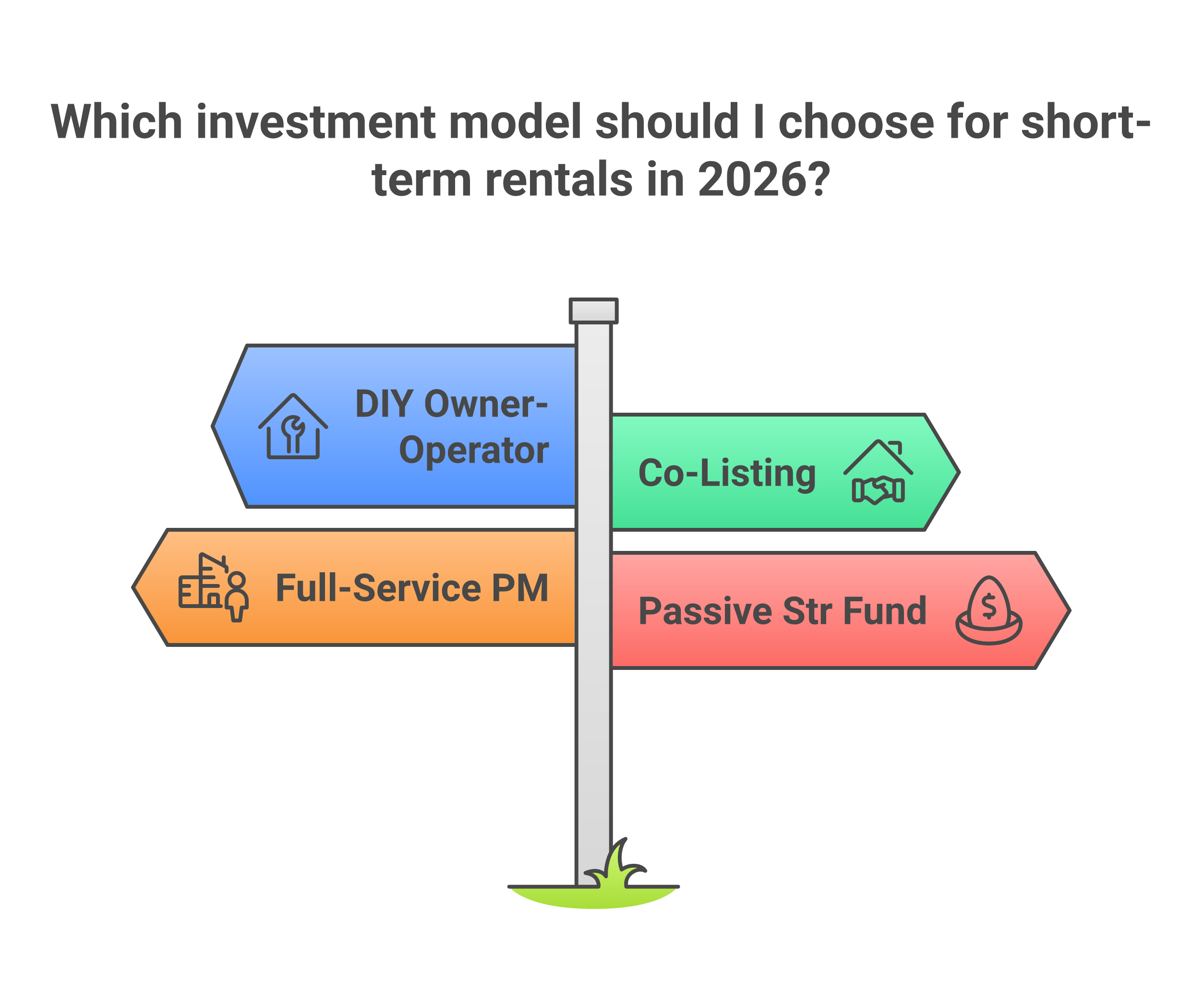

The four ways to invest in short-term rentals

Most online guides give you a single path and pretend it’s the only one. There are four, and the right one depends on whether you have capital, time, or both. I’ll cover each in detail below, but here’s the snapshot:

- Model 1, Buy and operate yourself (the DIY investment property approach): Capital required: $60K to $150K down payment plus furnishing and reserves. Time commitment: 5 to 15 hours per week per property. Best for: high earners who want full control, the OBBBA tax angle, and 12 to 25% all-in returns.

- Model 2, Co-listing (manage someone else’s short term rental for a revenue share): Capital required: $0 to $5K. Time commitment: similar to Model 1 but no ownership. Best for: people without capital who want to learn the operating model and earn passive income on someone else’s asset.

- Model 3, Full-service property management (the Vacasa or Evolve path): Capital required: same as Model 1. Time commitment: 1 to 3 hours per week. Best for: owners who want true hands-off but accept 25 to 45% revenue share with the property manager.

- Model 4, Passive short-term rental funds and syndications (earn passive income with capital, not time): Capital required: typically $25K to $100K minimums, accredited investor only. Time commitment: zero. Best for: high earners who want short term rental exposure without operating, but accept lower returns and 5-year capital lockups.

For most high-income W-2 professionals reading this, the right answer is Model 1 paired with a strong tax strategy. I’ll explain why under the OBBBA section below, but the short version is that Models 3 and 4 strip out the tax advantages that make short-term rentals worth doing for high earners in the first place.

Model 1: Buy and operate as a DIY investment property

The DIY investment property is the model that pays the highest returns and offers the strongest tax advantages, but it requires the most capital and time. You buy a property, furnish it, start renting it out on Airbnb and Vrbo, and operate it yourself or with a small team of cleaners and handymen renting out the property to guests on a rolling basis. You keep all the revenue minus operating expenses. You make the operating decisions. You own the asset. You research markets, compare price points, and decide what to buy.

How a DIY investment property cash-flows

The cash flow math on a DIY investment property is simple in theory: revenue minus operating expenses minus debt service equals net cash flow. The complexity is in the operating expense line, which is where most new investors miss the mark.

On a $400,000 short term rental generating $80,000 in annual revenue, expect operating expenses of $24,000 to $28,000. That covers cleaning costs at $80 to $150 per turnover (these are the maintenance costs and operating details that new investors miss) (figure 60 to 90 turnovers a year), supplies at $1,500 to $3,000, dynamic pricing software like PriceLabs or Beyond at $250 to $500 a year, channel manager subscriptions at $300 to $600 a year, utilities at $3,500 to $5,000, insurance at $1,200 to $2,500, and a maintenance reserve at 5% of gross rental income. After debt service of around $24,000 a year on a $320,000 mortgage, net cash flow lands at $20,000 to $32,000 a year before tax effects.

Capital required and operating expenses

Plan for a 20 to 25% down payment on an investment property because lenders price short-term rentals as higher risk than primary residences. On a $400,000 property that means $80,000 to $100,000 down. Add furnishing at $20,000 to $35,000, closing costs at $8,000 to $12,000, and three months of operating reserve at $7,000 to $10,000. All in, expect to need $115,000 to $155,000 in liquid capital before you take possession. For a side-by-side breakdown of the real startup costs across operating models, including the no-capital arbitrage path, see our budget comparison.

The interest rate on a typical investment property mortgage runs 0.5% to 0.75% above the rate on a primary residence. DSCR loans (debt service coverage ratio loans) are an alternative if your debt-to-income ratio is tight from your W-2 income, but they price 1 to 2 percentage points higher than conventional loans.

Why DIY ownership is the strongest investment strategy for the tax angle

The OBBBA short-term rental loophole only works if you are the owner and the operator. Hand the property to Vacasa or place capital in a fund and the tax advantages either shrink dramatically or disappear entirely. We’ll get into the detail below, but file this away: if you are reading this article because of the tax math, you almost certainly want to be in Model 1.

Model 2: Co-listing (manage someone else’s short term rental for a share of revenue)

Co-listing the vacation rental property of someone else is what 10XBNB students who lack starting capital begin with. Our full guide on how to become an Airbnb co-host walks through the operational playbook step by step. You partner with a property owner who has an under-utilized vacation home, a friend who can’t be bothered to operate their Airbnb, or a long term rental landlord who wants higher yields. You do all the work. You split the revenue, typically 10 to 30% to the co-lister depending on the scope of responsibilities.

Co-listing is the only model on this list that requires zero capital. It is also the fastest path to learning the operating side of the business without putting your own money at risk. Most students who later choose to invest more seriously in real estate by moving into real estate investing by buying their first investment property started by co-listing two or three rental properties first. After 6 to 12 months they understand the operating model, the dynamic pricing decisions, the guest communication patterns, and the seasonal rhythms.

The downside: you own no asset, you take no appreciation, and you get none of the tax advantages we discuss below. Co-listing is income, not investment. It is excellent income for some people, with active operators making $20,000 to $80,000 a year managing 3 to 8 properties. Operators who want to capture more of the upside often graduate to the related airbnb rental arbitrage model, where you sign the lease yourself and keep more of the spread. But it is not how you build long-term wealth.

Model 3: Full-service property management with companies like Vacasa or Evolve

Full-service property management is what most short term rental owners default to once they realize they don’t want the late-night guest texts. You own the property. A property management company handles guest communication, dynamic pricing, cleaner coordination, channel listings, maintenance dispatch, and review responses. You collect a monthly distribution check.

What a property manager actually does

A real full-service property manager runs the operating side of your business. They handle guest screening, the messaging from inquiry through checkout, dynamic pricing through PriceLabs or a proprietary engine, channel distribution to Airbnb and Vrbo, cleaner scheduling and quality control, supplies restocking, maintenance dispatch, and review responses. Done well, this is a real service worth paying for.

Done poorly, you pay 25 to 45% of revenue to someone whose pricing engine sets your rates lower than they should and whose cleaner shows up late twice a month. Property management quality varies enormously by company and by market.

The fee math on full-service property management

Vacasa charges 25 to 45% of gross revenue when add-ons are included. (For a similar breakdown of platform-side fees that property managers often pass through to owners, see our analysis of VRBO host fees.) Their base fee runs 25 to 35%, but cleaning markups, supply markups, maintenance markups, and damage waiver fees push the all-in rate higher than the headline number. Trustpilot reviews on Vacasa have averaged 2.1 out of 5 across many markets, and the company was acquired by Casago in May 2025.

Evolve sits at 10% of gross revenue on a leaner half-service model. Evolve handles the digital side including listing optimization, channel distribution, dynamic pricing, and guest messaging. They explicitly do not handle local operations like cleanings or maintenance. You hire those independently. Evolve’s Trustpilot scores have run higher, around 3.8 of 5, because the simpler value proposition tends to meet expectations when owners understand the model upfront.

On an $80,000 STR, Vacasa takes $20,000 to $36,000 a year. Over a 10-year hold that is $200,000 to $360,000 paid out to the property manager. Evolve takes $8,000 a year, or $80,000 over 10 years. Self-managing with a one-time $4,000 training program and a $2,000 a year toolset works out to $24,000 over 10 years, plus the time you put in. The math is rarely close.

When using a property management company makes sense

Property management makes sense for owners who genuinely cannot put in any time, are far enough from the property that cleaner and contractor relationships are impractical, or have so many properties that scale demands a team. For most W-2 professionals operating 1 to 3 properties (or rebalancing an investment portfolio that is too heavy in equities) within a 4-hour drive, the math favors self-managing.

Model 4: Passive short-term rental funds and how to earn passive income with capital instead of time

Passive short-term rental funds let you earn passive income from short-term rentals without operating any property. You provide capital. The fund acquires, designs, furnishes, and operates a portfolio of properties. You receive quarterly or annual distributions plus a share of the eventual sale proceeds.

How passive short term rental investments work

Most passive short term rental vehicles are 506(c) syndications structured as Reg D offerings under SEC rules. You commit capital, the fund deploys it across multiple properties, and you receive a preferred return (typically 8 to 10%) plus a share of profits above that hurdle. The general partner running the fund takes a 1 to 2% management fee and 20 to 30% of profits above the preferred return.

TechVestor is the most visible name in this category in 2026. Their minimum investment is $25,000 and they require accredited investor status. Independent reviews on BiggerPockets, Physician on FIRE, and NewSilver report cash-on-cash returns in the 8 to 12% range with a 5-year capital lockup. The fund focuses on 4 to 6 bedroom homes in high-yield STR markets. Awning runs a different model focused on white-glove acquisition for individual investors. Pacaso operates in the co-ownership category with shared luxury second homes.

Minimum investments and accreditation

Most passive short term rental vehicles require accredited investor status. The SEC defines accredited investor as someone with $200,000 in individual income for the past two years ($300,000 if filing jointly), or net worth above $1 million excluding primary residence. Minimum investments range from $25,000 at the low end to $100,000 or more at the higher end.

Capital is locked up for 3 to 7 years on most short term rental funds. You cannot pull out. If the fund underperforms, you cannot pay your way out and your only choice is to wait for liquidation.

Real returns vs marketing claims on passive short term rental funds

Reported returns on passive short term rental funds run 8 to 12% blended cash on cash according to multiple third-party reviews. Sponsor track records vary. Investors should review the principals’ prior ventures, do your own research on the real estate investment thesis, audited financials where available, and forum threads on BiggerPockets where current and former limited partners post candid reviews.

Compared to Model 1, passive short term rental funds offer roughly half the cash-on-cash return, none of the meaningful tax advantages (depreciation passes through but is limited by passive activity loss rules unless you qualify for material participation, which you cannot in a passive fund), and a multi-year capital lockup. They are appropriate for accredited investors who want pure exposure without operating, but for most W-2 high earners with the time to operate one property, Model 1 wins on every dimension.

The OBBBA tax angle: the strategy nobody else is teaching

Renting out a short term rental property has unique tax treatment that most online guides miss. This is the section that converts a curious reader into someone who actually buys an investment property. If you take nothing else from this article, take this section.

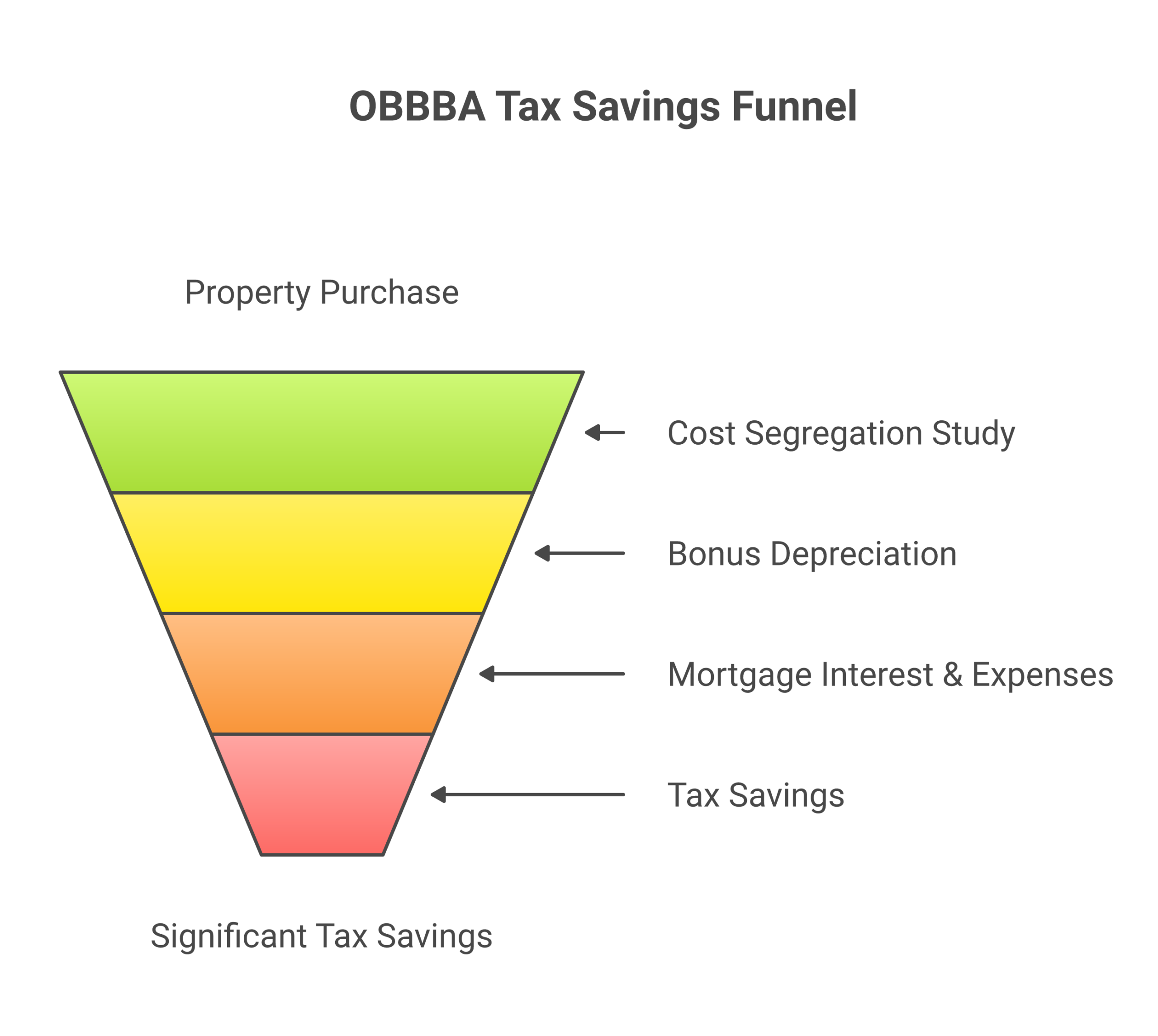

What OBBBA does and why it matters for short-term rental investors

The One Big Beautiful Bill Act, signed July 4, 2025 as Public Law 119-21, permanently restored 100% first-year bonus depreciation for qualified property acquired after January 19, 2025 (per official IRS guidance). Before OBBBA, bonus depreciation was on a phaseout schedule that would have dropped to 20% by 2026 and 0% by 2027. The new law brought 100% back and made it permanent. For real estate investors, this is one of the most significant tax changes in a decade.

Bonus depreciation alone does not help most W-2 professionals. The benefit is locked behind the passive activity loss rules, which prevent rental losses from offsetting active income like W-2 wages. To unlock the benefit, you have to do one of two things: qualify as a real estate professional (Real Estate Professional Status, or REPS), or operate a short-term rental that qualifies for the short term rental loophole.

How the short-term rental loophole works for W-2 professionals

The short-term rental loophole is a quirk in the tax code that reclassifies certain rentals as a trade or business rather than a passive activity. The mechanism: if the average period of customer use is seven days or less, your rental is no longer treated as a passive rental for tax purposes. Combined with material participation, the losses pass through to offset your W-2 income.

For high-income professionals, this is the unlock. You don’t need to be a real estate agent, a property manager of long term properties, or a full-time real estate professional. You don’t need to spend 750 hours a year in real estate. You need to operate a short-term rental that books for an average of seven days or less per stay (most short-term rentals do this naturally) and you need to materially participate in the operation.

Material participation: the 100-hour and 500-hour tests

Material participation has seven tests under IRS rules but for short-term rental investors there are really only two that matter:

- The 500-hour test: You participate in the activity for more than 500 hours during the tax year.

- The 100-hour test: You participate for more than 100 hours during the year, and no other individual participates more than you do.

Most W-2 professionals with one or two short-term rentals comfortably hit the 100-hour threshold. Activities that count include guest communication, pricing decisions, listing optimization, cleaner coordination, supplies management, maintenance scheduling, and reviewing financials. Activities that do not count include time spent reading books on short term rental investing or browsing AirDNA reports.

Document everything. The IRS audits material participation claims, and the ones that fail audit are almost always the ones with no contemporaneous logs. Keep a simple spreadsheet with date, activity, time spent, and brief description.

Cost segregation studies: turning a property into a tax shield

Standard tax depreciation on a short-term rental property runs 39 years for non-residential or 27.5 years for residential rental property under MACRS (the formal rules are in IRS Publication 946). That spreads the depreciation deduction thin across decades. Cost segregation reclassifies components of the building into shorter-life categories: 5-year property (furniture, appliances, decor), 7-year property (some interior fixtures), and 15-year property (landscaping, paving, exterior improvements).

Once reclassified into shorter lives, the components qualify for 100% bonus depreciation under OBBBA. A typical cost segregation study on a $400,000 short term rental will reclassify 20 to 35% of the property’s basis into 5, 7, and 15-year property. That means $80,000 to $140,000 of the building’s basis becomes immediately deductible in the year the property is placed in service.

Worked example: $400,000 short-term rental and the year-one tax savings

Here is the math on a real case. A high-income professional buys a $400,000 short term rental with a $320,000 mortgage and $80,000 down. Cost segregation reclassifies $120,000 of the basis (30%) into 5, 7, and 15-year property. Under OBBBA’s 100% bonus depreciation, that $120,000 is fully deductible in the first year. Add normal expenses (mortgage interest of around $18,000, operating expenses of $24,000) and you have a paper loss approaching $40,000 on top of revenue.

For a W-2 earner in the 40% combined federal and state bracket, that paper loss flowing through to offset W-2 wages saves $16,000 in taxes in year one (combining federal income taxes plus state income taxes). On a more aggressive cost segregation study reclassifying $170,000 of basis, year-one savings can hit $30,000 to $35,000. On a $600,000 property the same math produces $40,000 to $60,000 in year-one tax savings.

Combine the year-one tax savings with the recurring cash flow ($20,000 to $32,000 on this property), the appreciation potential, and the personal use option, and you have an investment that compounds in ways stocks and bonds simply cannot. This is why high-income professionals who understand the math are buying short-term rentals in 2026 rather than maxing out their 401(k) backdoor Roth.

One important caveat. The depreciation recapture happens when you sell. The IRS gets some of that money back at sale. The tax savings are real but they are also a deferral, not pure forgiveness. If you hold long-term and 1031 exchange into the next property, you defer indefinitely. Talk to a real estate investment-specialized CPA before structuring anything.

Capital required by investment strategy

Different models, different capital requirements. Here is the realistic picture:

- DIY investment property (Model 1): $115,000 to $155,000 liquid required. Down payment, furnishing, closing costs, operating reserves. Best for high earners who can save aggressively or who already have liquid capital.

- Co-listing (Model 2): $0 to $5,000. The $5,000 covers tools (PriceLabs, channel manager, basic CRM), a possible course or training, and minor working capital. Best for those without capital who want to learn the model first.

- Full-service property management with Vacasa or Evolve (Model 3): Same as Model 1 since you still own the property. The property management company is paid out of operating revenue, not upfront. Capital requirements identical to DIY.

- Passive short term rental investments (Model 4): $25,000 to $100,000 minimum, accredited investor only. Best for high net worth individuals who want short term rental exposure without operating.

The model most relevant to the typical high-income W-2 professional reading this is Model 1, with Model 2 as a viable on-ramp for those building toward Model 1. Models 3 and 4 trade away the tax benefits that make this asset class worth the work in the first place.

How to invest in short-term rentals: the step-by-step path from W-2 to first cash-flowing STR

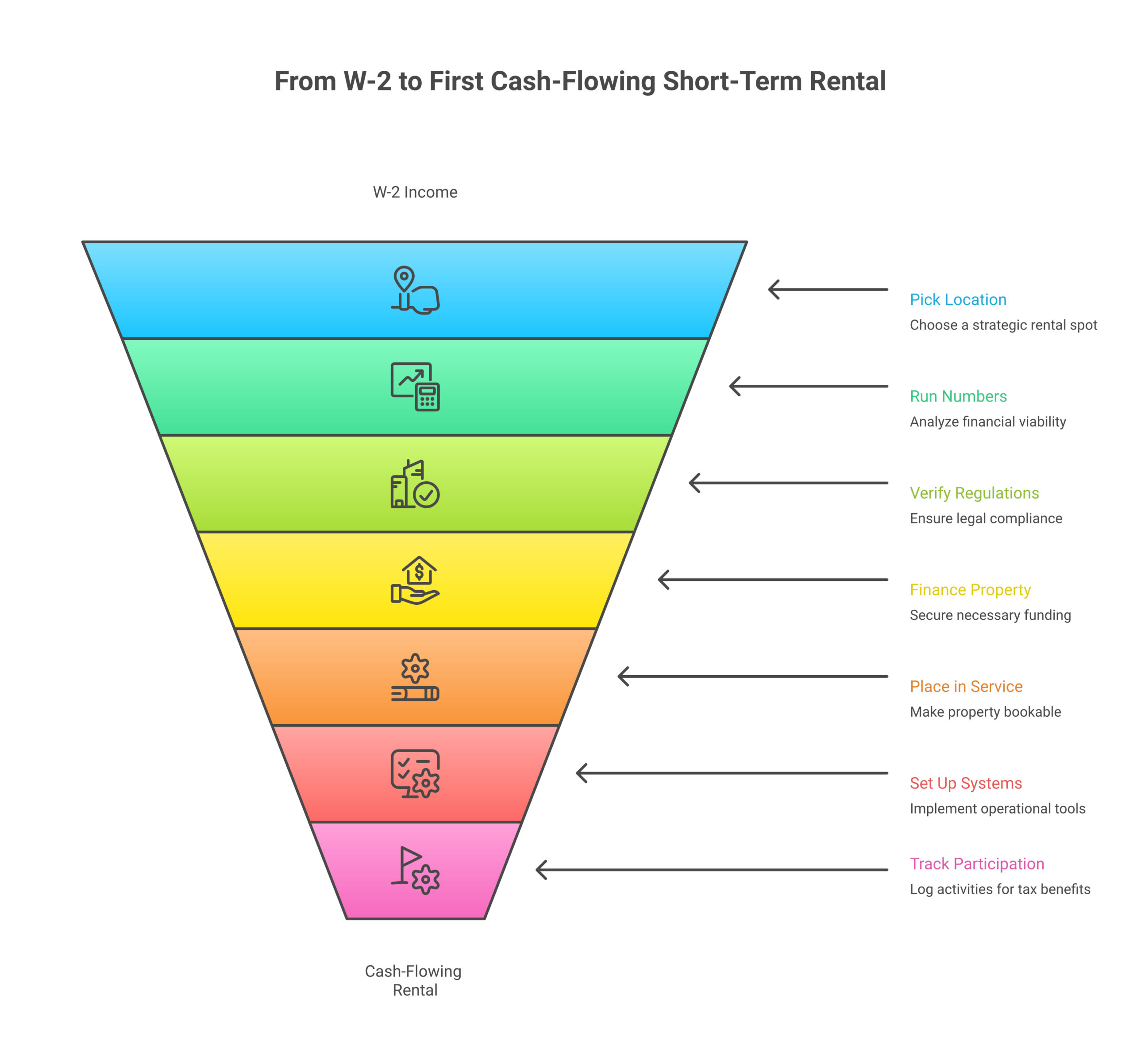

Here is the actual playbook I take students through for buying a first investment property under the OBBBA strategy:

Step 1: Pick a great location with consistent high demand

The best vacation rental markets in 2026 share three traits: year-round high demand (not just one tourist season), reasonable purchase prices relative to income, and STR-friendly local regulations. Port Arthur Texas is a contractor and industrial demand market with $35K average annual revenue potential and 67% occupancy rates (per AirDNA). Scottsdale runs higher absolute revenue with higher purchase costs. Mid-size cities like Columbus Ohio, San Antonio, and Chattanooga consistently outperform tourist-heavy markets where price competition is bid up by everyone. See our deeper analysis on the most profitable Airbnb cities ranked by data and our 2026 best Airbnb markets report for current rankings. The single best piece of advice I can give a new investor is this: pick the great location first, run the numbers second, fall in love with the property third. Most investors do this in reverse and pay for it.

Step 2: Run the numbers using actual ADR and occupancy rates

Research and pull comparable rental property data from AirDNA, Rabbu, Mashvisor, or a free tool like the Airbnb listing search itself. Look at rental properties with 3 or more bedrooms in your target neighborhood with strong reviews. Calculate average daily rate (ADR) and occupancy rates from the past 12 months of bookings, not the headline marketing number. Multiply ADR times occupancy rates times 365 to get gross rental income. Subtract operating expenses at 30 to 35% of gross. Subtract debt service. The remainder is what you cash-flow. Smart real estate investors run the math three times with different occupancy rate assumptions before they decide on a purchase.

Step 3: Verify local regulations before signing anything

Many cities have STR-specific permits with licensing fees, occupancy caps, or outright bans on non-owner-occupied short-term rentals. Verify the regulations in writing from the city or county website before you submit an offer. Talk to a local real estate agent who specializes in short term rentals, ideally one who knows the local market, the dynamics of vacation rentals in your target market, and the regulations affecting your target market well. They will know the gotchas. Some markets that look great on paper have HOA rules or neighborhood covenants that prohibit short-term rentals even where city law allows them.

Step 4: Finance the rental property correctly

Conventional investment property loans require 20 to 25% down and 0.5 to 0.75% above primary residence rates. DSCR loans qualify based on the rental property’s projected cash flow rather than your DTI ratio, useful if your W-2 income is high but already supporting other debt. Research two or three lenders for your real estate investment financing and compare price quotes carefully. Some lenders are aggressively pricing short term rental investors right now while others are pricing them as higher risk. The price difference between lenders on the same purchase can be 0.5 to 1.0 percentage points, which works out to thousands of dollars per year in interest expense.

Step 5: Place into service before year-end for OBBBA timing

The OBBBA bonus depreciation kicks in for the year a property is “placed in service,” meaning it’s available and ready for guest bookings. If you close in November and have it listed and bookable by December 31, you take the year-one bonus depreciation in that tax year. If it’s not ready until January 2 of the following year, you wait 12 months for the tax benefit. Plan your closing and furnishing timeline accordingly.

Step 6: Set up operating systems before your first guest

You need a small stack of operating tools: dynamic pricing software like PriceLabs or Beyond (compared in our PriceLabs vs Beyond review), a channel manager to push the listing to Airbnb and Vrbo simultaneously, a guest messaging system, a cleaner schedule, supplies tracking, and a maintenance reserve account. Set these up before you take your first booking. Trying to build them while juggling guests is how new operators burn out.

Step 7: Track everything for the material participation test

From day one, log every minute you spend on the property in a simple spreadsheet. Date, activity, time, brief description. This is your audit defense for the material participation test that unlocks the OBBBA tax benefit. Most operators easily clear 100 hours a year on one property when they actually count their time.

Common mistakes high-income professionals make when investing in short term rentals

These are the mistakes I see repeated quarter after quarter from new investors:

- Buying the wrong property in the right market. Solid markets have soft sub-pockets. Two streets over from the booking-loaded blocks can mean half the occupancy. Rely on AirDNA neighborhood-level data, not city-level averages.

- Underestimating operating expenses. New investors underestimate cleaning costs, supplies turnover, and maintenance. Budget at 30 to 35% of gross, not the 20% you see in optimistic proformas.

- Skipping the cost segregation study. A $4,000 to $8,000 cost segregation study on a $400,000 property unlocks $20,000 to $35,000 in year-one tax savings. Skip it and you leave that money on the table.

- Failing the material participation test for lack of records. The IRS audits this aggressively. Without contemporaneous logs you lose at audit even if you actually did the hours.

- Hiring a generalist CPA who doesn’t know real estate. Generalist CPAs miss cost segregation, miss the short-term rental loophole, and apply passive activity loss rules incorrectly. Hire a real estate investment-specialized CPA who can review the details of your property and tax situation. The fees are higher and the savings cover the difference 50 times over.

- Choosing full-service property management without doing the math. Vacasa at 35% on an $80,000 property is $28,000 a year you don’t keep. Most professionals can self-manage one property in 5 to 10 hours a week. The hourly rate on managing your own short term rental works out higher than most W-2 jobs.

- Treating it like passive income from day one. The first 6 to 12 months are operationally heavy. After systems are in place, hours per property drop dramatically. Plan for the ramp.

How to invest in short-term rentals: final thoughts

Short-term rentals in 2026 are a genuine investment for the high-income W-2 professional who is willing to put in 5 to 15 hours a week and willing to use the tax code the way it was written. The OBBBA bonus depreciation provision combined with the short term rental loophole produces year-one tax outcomes (across federal income taxes, state taxes, and self-employment taxes) that most equity portfolios cannot match. Self-management beats property management on every financial dimension when you operate one or two properties. Co-listing is the on-ramp for those without capital. Passive short term rental funds make sense for accredited investors who specifically don’t want to operate.

The investors I see succeed treat the first property like a small business: they pick the location with discipline, they verify local regulations, they finance it conservatively, they place into service for the OBBBA tax window, they track their hours for material participation, and they hire the right CPA. None of this is complex. Most of it is uncommon because most online guides skip the tax depth that turns this asset class from interesting to compelling. If you want a structured curriculum that walks you through the full operating model and the OBBBA tax angle, our review of the best Airbnb courses in 2026 is the place to start.

Frequently Asked Questions about how to invest in short-term rentals

Is investing in short-term rentals really passive income?

No, not in the strict sense. Earning passive income from real estate without active work is only possible through Model 4 (passive short term rental funds) or by paying a property manager 25 to 45% of revenue. For Model 1 (DIY ownership), expect 5 to 15 hours a week per property in steady state, with the first 6 months running higher. That said, the IRS treats your short term rental as an active trade or business under the short-term rental loophole, which is what unlocks the most valuable tax advantages.

How much money do I need to invest in my first short term rental?

For renting out a property you buy yourself (Model 1), plan on $115,000 to $155,000 in liquid capital for a $400,000 property: 20 to 25% down, $20,000 to $35,000 furnishing, $8,000 to $12,000 closing, and 3 months operating reserves. For co-listing (Model 2), $0 to $5,000 covers tools and training. For passive short term rental funds (Model 4), minimums start at $25,000 with accredited investor status required.

What is the OBBBA short-term rental loophole?

The One Big Beautiful Bill Act restored 100% bonus depreciation permanently for property acquired after January 19, 2025. Combined with the short-term rental loophole (rentals with average customer stays of seven days or less are treated as a trade or business, not passive rentals), high-income W-2 professionals can offset W-2 wages with first-year paper losses on short term rental investments. A $400,000 property paired with a cost segregation study commonly produces $40,000 to $60,000 in year-one tax savings for a high earner.

Do I need real estate professional status to use the bonus depreciation?

No. Real Estate Professional Status (REPS) requires 750 hours a year in real estate trades or businesses and more than half your work time, which most W-2 earners cannot meet. The short-term rental loophole is the alternative path: average customer stays of seven days or less plus material participation (100 or 500-hour tests) qualifies you to use rental losses to offset W-2 wages without REPS.

Are short term rentals still profitable in 2026?

Yes, in well-chosen markets and with disciplined operating. The US short term rental market is $72 billion in 2025 and growing 7.4% annually. Properties bought right return 10 to 15% cash-on-cash. The investors I see fail are not victims of market conditions; they are people who paid too much for the property, underestimated operating expenses, or chose markets based on tourist appeal rather than actual booking data.

How does Vacasa or Evolve compare to self-managing?

Vacasa typically charges 25 to 45% of revenue when add-ons are included. Evolve charges 10% on a leaner half-service model. Self-managing with a basic toolset (PriceLabs, channel manager, simple CRM) costs about $2,000 a year plus your time. On an $80,000 short term rental over 10 years, that’s roughly $200,000 to $360,000 to Vacasa, $80,000 to Evolve, or $20,000 to self-manage. Self-management wins for most professionals operating 1 to 3 properties.

What occupancy rates and average daily rates should I model?

Pull actual data from AirDNA or Rabbu for properties with 3 or more bedrooms in your target neighborhood with strong reviews. National average occupancy in 2026 is around 60%. Top markets like Port Arthur Texas hit 78%. Be conservative in your underwriting: model the realistic case at 60% and the bad year at 50%. ADR varies enormously by market, ranging from $120 to $180 in mid-tier markets to $300+ in premium markets.

Should I buy a single-family home or a condo for my first STR?

Single-family homes outperform condos on cash flow in most markets because of guest appeal (multiple bedrooms, private outdoor space, no shared walls), no HOA restrictions on rentals, and lower per-square-foot acquisition cost in suburbs. Condos win in vertical urban markets where land is scarce, but HOA restrictions on short-term rentals are increasingly common. Verify the HOA rules in writing before any condo offer.

What are the biggest risks to investing in short term rentals in 2026?

Three real risks: regulatory tightening (cities adding short term rental caps or bans), oversupply in saturated markets that pressures both ADR and occupancy, and macro demand softness if a recession hits. Mitigate regulatory risk by choosing markets with stable, written STR-friendly rules. Mitigate oversupply by avoiding the 10 most-saturated tourist markets. Mitigate macro risk by buying properties that cash-flow at 50% occupancy as your stress case.

How do I get started if I have a great location in mind already?

Run the numbers on three specific properties in that market using actual AirDNA data, verify local regulations in writing, talk to two lenders to lock in financing, and engage a real estate-specialized CPA before you write an offer. Most of the work happens before the closing, not after. The W-2 professionals I see succeed are the ones who treat the first property purchase like a business decision rather than a real estate transaction.

source https://learn.10xbnb.com/how-to-invest-in-short-term-rentals/

No comments:

Post a Comment